State of the Industry: 2025-2026

Written by David C. Lester, Editor-in-Chief

Photo courtesy Justin Franz.

ATLANTA - Editor-in-Chief David C. Lester writes about the state of the rail industry as we transition from 2025 to 2026.

The organization of the industry has been the sharp focus of railroad planners during the past year. All this work is supposedly for the benefit of the industry itself, customers, shareholders, railroad employees, and the country. The only intent to file for merger approval has come from Union Pacific and Norfolk Southern. Will this merger be approved? If it is, how will the rest of the industry react? Will the response be a highly touted BNSF+CSX merger, essentially creating two parallel U.S. transcontinental railroads? If UP+NS is or is not approved, might other combinations make sense?

There is a tremendous amount to unpack from these questions, and the Surface Transportation Board will examine them in 2026 in hearings and deliberation around what it believes is best in light of the “new” 2001 merger rules. Moreover, thorough examination of key factors that can grow rail traffic, such as customer service quality, competitive rates, reciprocal switching, and improved marketing efforts on the part of Class Is will be front and center during the process.

In addition to mergers, there are other areas to consider as we evaluate the year about to end and look ahead to the one that’s about to begin. Let’s look at these in some detail.

Industry Organization

As we wind up 2025 and look ahead to 2026, the rail industry finds itself at a crossroads. The number one concern in the industry, just below safety and traffic growth, is its organization. By the time you read this, Union Pacific and Norfolk Southern will likely have submitted their merger application to the Surface Transportation Board (STB). The coming year promises to be an interesting one as the STB reviews the application and evaluates feedback and commentary from various parties, including other railroads and shippers. If successful, the merger will significantly reshape the industry and will likely prompt a competitive response of some sort. Most believe that the only sensible transaction would be the merger of BNSF and CSX, which would provide two transcontinental railroads and bring the total number of North American Class I roads to four.

Significant comments from other Class I railroads have already hit the news. For example, on its website, BNSF says:

“This potential merger could have widespread effects on rail competition, supply chains and service reliability through North America. It is important that the Surface Transportation Board hear from you now and at every opportunity during the regulatory review process. Your views matter and will help them make informed decisions. Here is how you can tell the STB to say no to unchecked market power and the loss of competitive options you’ll never get back.”

Certainly, no doubt about how “Berkshire,” as UP CEO Jim Vena likes to call it, feels about the merger.

CPKC’s President and CEO Keith Creel is not happy about, nor is interested in being involved in, any merger. Railway Age Contributing Editor Justin Franz reported in Railfan & Railroad in August that Creel said “We believe that a transcontinental merger would trigger permanent restructuring of the industry and result in a disproportionately large railway whose size and scope would require others to take action. This will likely result in an unnecessary wave of railway mergers that today is not the best way to support American businesses nor the public interest and has the potential to create more issues than it solves.”

For its part, CSX is not commenting on the merger, although the dismissal of former President and CEO Joe Hinrichs and replacement with Steve Angel, who has experience with mergers and acquisitions in other industries, tells you what CSX wants to do. However, BNSF has stated that it is not interested in participating in a merger. Of course, that may change if UP+NS is approved. Nevertheless, both (BNSF-CSX) railroads have initiated cooperative international and domestic intermodal service in the past few months. While single-line service is one of the major reasons for and purported benefits of transcontinental mergers, it will be interesting to see if the BNSF-CSX service truly reduces travel time and improves volumes. CPKC initiated some similar services after its merger and is beginning to see significant increases in international volumes.

The Canadian National position is a bit tougher to read because its comments about the proposed merger have included statements of fact, but they’re non-committal. For example, the CN website shares this statement: “This transaction could have far-reaching implications for rail competition, supply chains, and service reliability in North America. CN will be actively participating in the STB review of this proposed merger.” The railroad has also championed the notion that “our customers’ voices should be heard.” OK, all of this is fine, but what’s the railroad’s position on UP+NS? One would assume that CN is against the merger but cannot definitively conclude that based on the statements the railroad has released to this point. The message seems to be limited to “customers should be heard,” “the merger has far-reaching implications,” and “we’re monitoring it carefully.” Perhaps we’ll get more clarification going forward. Although, might CN be interested in a merger of its own?

As expected, most shippers and shipper organizations are not enthusiastic about UP+NS. For example, the National Industrial Transportation League (NITL) said in a statement this summer that “NITL has consistently been on the record as opposing further consolidation in the freight rail industry . . . Despite the promises that rail customers would benefit from mergers through more efficient service, in reality captive rail customers must pay increasingly higher prices for unreliable and inadequate service.” In a similar vein, the American Chemistry Council says that “The American Chemistry Council (ACC) and its members are deeply concerned that the proposed merger between Union Pacific (UP) and Norfolk Southern (NS) will result in more [harm to] the U.S. freight rail industry. We urge policymakers and regulators to reject any rail merger that does not clearly enhance competition and

improve service.”

It comes as no surprise that both Union Pacific and Norfolk Southern shareholders have approved the proposed merger. An interesting twist on UP’s part is President and CEO Jim Vena’s recent lobbying of the White House on behalf of the merger, as well as UP’s contribution to funding the new White House ballroom. Some looked askance at this since it is up to the independent STB to approve or reject the merger application and is not (supposedly) subject to political pressure. Yet, in firing STB board member Robert E. Primus, a Democrat, in August, POTUS 47 is the first U.S. president to fire a member of either the Interstate Commerce Commission (the predecessor organization of the STB) or of the STB itself, so it’s hard to say what that may mean as the approval process develops. However, the chairman of the STB, Patrick J. Fuchs, is widely respected by nearly everyone involved with or affected by the merger, and he is not likely to easily succumb to political pressure, if it even comes.

Some say, however, that given the political climate at the moment, Vena would have been foolish not to solicit White House support for the merger. At a recent press conference, Vena said the ballroom donation made to the National Park Service (NPS) is in line with a long relationship with the NPS, going back to the days when Union Pacific initiated an advertising campaign to attract Americans to visit some of the newly opened national parks. The NPS is responsible for maintaining the White House grounds.

Rail Traffic Review

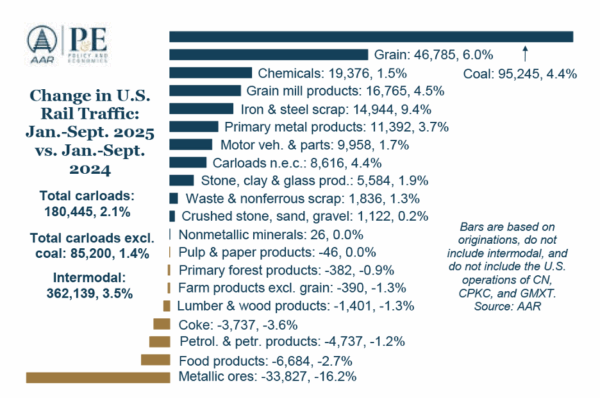

As is usually the case, rail traffic year-to-date as of September 30 is a mixed bag. According to the Association of American Railroads Policy & Economics unit, total U.S. carloads from Jan.-Sept. 2025 are up by 2.1%, which equates to 180,455 carloads, over the same period in 2024. When coal is removed from the analysis, the carloads during the same period (Jan.-Sept. 2025 vs. Jan.-Sept 2024) were up 1.4%, which equates to 85,200 carloads. The AAR also reports that from Jan.-Sept. 2025, compared to the same period in 2024, intermodal volume (which includes containers and trailers) was up 3.5%, equating to

362,139 units.

Total U.S. rail volumes for Jan.-Sept. 2025 were: total carloads, 8.65 million, total carloads excluding coal, 6.37 million, and total intermodal units, 10.57 million. The graphic on the next page, courtesy of Railway Age and the Association of American Railroads Policy and Economics unit, provides a detailed breakdown of changes in rail traffic commodity groups for Jan.-Sept. 2025 vs. Jan.-Sept. 2024.

Rail Passenger Considerations

While there are other segments of the passenger rail industry, we’re focusing on Amtrak, Brightline, and high-speed rail. While the reports on each are a very mixed bag, it’s worth noting that Kevin J. Holland, the editor of the quarterly Passenger Train Journal, points out in his editorial for the Q4 issue that “all too often, the attitude of [passenger operators] is ‘You’re lucky to have any service, so quit whining.’” For example, he cites the windowless seat rows on Amtrak’s NextGen Acelas, quoting one Reddit commentator’s point that “You can’t advertise the view as one of the amenities of train travel if they don’t provide a window!” With that unvarnished commentary, let’s move on to the “official” review of Amtrak.

Amtrak recently released a report touting its success during FY2025 (Oct. 2024-Sept. 2025), with a second consecutive year of increased ridership. The agency reports it provided 34.5 million customer trips during the year, which set all-time records for both ridership and revenue. Here are some additional achievements for the year reported by Amtrak:

Ridership: 34.5 million customer trips, a 5.1% increase over FY24 and an all-time record.

Adjusted Ticket Revenue: $2.7 billion – a first in Amtrak’s history and 10.4% higher year-over-year.

Total Operating Revenue (Includes payments from state partners for State Supported routes): $3.9 billion, a 9.1% increase over FY24.

Customer On-time Performance: Northeast Regional trains reached their highest on-time performance in recent years this September.

Customer Service: Surpassed systemwide customer service goals, with historical bests in Wi-Fi, food and beverage, train status communications, and station signage.

Miles Traveled: Amtrak passengers logged 6.9 billion miles in FY25, a new all-time high.

New Services, New Trains: Made history with the launch of Amtrak Mardi Gras Service along the Gulf Coast and NextGen Acela on the Northeast Corridor; Borealis service drew over a quarter million riders in the Midwest since its FY24 debut.

Capital Investments: Record $5.5 billion – up nearly 25% year-over-year – in major projects and state-of-good-repair initiatives.

Adjusted Operating Earnings (Unaudited): Improved by 15.1% over FY24 to ($598.4 million), on track to achieve train operational profitability by FY28.

Given that Amtrak’s history has been fraught with bad news, poor performance, and lack of support, this data points to positive trends.

These days, a reference to Brightline includes Brightline Florida and Brightline West. However, the company, which began with such promise and excitement, has run into some choppy air on both sides of the country. Brightline Florida, for example, according to reporting by Railway Age’s Contributing Editor, David Peter Alan, booked 3 million trips in 2024 but lost almost $550 million in 2024. You can read David’s report, published in September, at this web address: https://www.railwayage.com/passenger/intercity/brightline-loses-nearly-550mm-in-2024-but-keeps-on-going/. David followed up in November, reporting that “There have been more indications of trouble for Brightline since then, including skyrocketing costs for building Brightline West in the Mojave Desert of Southern California and Brightline’s own action of slashing service between its South Florida stations and Orlando Airport.” You can read David’s latest report at the web address https://www.railwayage.com/passenger/high-performance/brightline-financial-woes-continue/?RAchannel=news.

For the October 2022 issue of Railway Age, the then RT&S managing editor prepared a feature story on Brightline and its pending operation to Orlando from Miami. We were fortunate to travel to Miami and have a complete tour of stations, maintenance facilities, and a ride from Miami to West Palm Beach. It was a great experience and we found the company very impressive, leaving with the thought “if anybody can do it, these guys can.” RT&S and Railway Age continue to wish Brightline well, but we’re concerned about the financial situation at the company, especially its recent ask of the POTUS 47 administration for a $6 billion federal loan for Brightline West. While the cost of construction is expensive, the even larger worry is that even with strong ridership in Florida, the company has lost money and reduced service. Arranging financing for construction is one thing; losing big bucks on operation is quite another.

The RT&S editor has written in the past that the massive construction cost increases for building high-speed rail systems, including the California High-Speed Rail system projected to provide service between Los Angeles and San Francisco, are dampening support for high-speed rail, at least for the time being. Moreover, the lack of political support for funding the CHSRA from the administration, and pulling previously committed federal funds for it have made things even worse. We’ve about reached the point of throwing up our hands on U.S. high-speed rail. While we would like to see it, we’ve written before that the money may be better spent on improving conventional Amtrak, commuter rail, and rail transit. Many hi-speed advocates write and talk about it until they’re blue in the face, but nothing ever seems to significantly move forward. Right now, all we have to show for the CHSRA project is a support infrastructure, sans track and trains, sitting in the Central Valley of the state.

The U.S. Economy

Analyzing and predicting the path of the U.S. economy is almost like counting and predicting the total number of raindrops falling in your backyard during a thunderstorm. And this is on a good day. Exacerbating this challenge in 2025 is the uncertainty around U.S. trade policy (mostly tariffs imposed by the Executive Branch) and the recent government shutdown.

The Policy and Economics unit at the AAR says the U.S. economy “continues to defy expectations with its resilience” as we move through the fall. Moreover, it says “projections vary widely, a sign that conflicting economic signals have made forecasting more difficult amid shifting consumer behavior, policy uncertainty, and uneven sectoral performance.” According to the U.S. Bureau of Labor Statistics (BLS), the Consumer Price Index (all items) rose 3.0% for the 12 months ending September 2025, after rising 2.9% over the 12 months ending August 2025. The all items less food and energy index also rose 3.0 percent over the last 12 months, according to the BLS. The “all items less food and energy” numbers do not include energy and food because prices of those commodities are often subject to wider swings and can skew the overall inflation rate. However, the BLS reports that food prices increased 3.1% and energy costs rose 2.8% during this period. Drilling down on energy costs, BLS says “Within energy, the natural gas prices rose 11.7% over the year and electricity costs increased 5.1%. In contrast, gasoline prices were 0.5% lower than a year earlier.” Taken together, the 3% inflation rate has not been strong enough to motivate Fed interest rate cuts, although the agency did make a quarter-point cut in September, the first since December 2024, because earlier this year, job reports showed significant slowing. Yet, the September jobs report, released after a seven-week government shutdown, surprised most economists. The expectation was an increase of about 50,000 jobs in September, but the reported number was over double that –119,000 jobs added in September. This has many economists thinking that the Fed will forego another rate cut in December.

Consumer spending and confidence, according to the AAR, are important for railroads. “For freight railroads, customer-driven volumes, especially intermodal shipments, often mirror [shifts in income, inflation, and job prospects], making trends in spending and confidence key indicators for railroads to monitor.” The AAR points out, though, that the spending numbers are more important because the correlation between confidence and spending can vary in strength. AAR reports that the consumer confidence index “fell from 97.8 in August to 94.2 in September, a five-month low and a continuation of a downward trend since November 2024 when it peaked at 112.8.” Conversely, AAR reports that “total inflation-adjusted consumer spending in August was up 0.3% over July, about the same increase as the prior two months. The year-over-year gain in August was 2.7%, the most in four months.”

Global Concerns

While U.S. business conditions can be impacted by world events in the political, military, medical, and economic arenas, unless there is a major catastrophe in any of these areas, most observers do not base rail industry forecasts and outlooks on them. However, there are several issues worth noting.

While there is currently a tenuous ceasefire between Israel and Hamas, with control of Gaza divided between both, there have been violations of the ceasefire agreement. The larger concern for the moment is what it will take to rebuild Gaza and return its people to some semblance of an orderly life. It is doubtful that rebuilding plans put forth by the United States, Israel, and Arab states will see approval soon, if at all. And there is always the distinct possibility of abandonment of the cease fire and resumption of fighting.

The war between Russia and Ukraine continues. The death and destruction levied against both countries has been horrific, and there is no end in sight. The Economist recently reported that a peace deal, allegedly developed jointly by the United States and Russia, would be crippling to Ukraine. The chances of this being adopted are virtually non-existent, according to most observers. Moreover, Ukraine president Volodymyr Zelensky recently learned that several of his government’s officials have stolen millions of dollars from the state nuclear agency, a discovery which left Zelensky, according to The Economist, “floored.” Clearly, a continuing mess. Likely the greatest risk is that one party in the conflict could introduce short-range nuclear weapons in the fight, which would have disastrous consequences for the world at large.

Tensions between major world powers continue to plague us, which is not new. One element now entering the mix is the development and use of artificial intelligence (AI) around the world. Extremely powerful, AI can bring about a lot of good for mankind, as it has for the railroad industry and other sectors of the world economy. Now that the genie is out of the bottle, though, AI is just as available to those who would do harm as it is to those interested in using it for progress. That’s way beyond the scope of our analysis but something worth keeping in mind.

Political divisions in the United States continue to be a concern. While this has resulted in uncertainty around trade policy and long-term planning for industry, the U.S. economy is showing a fair amount of resiliency. Yet, this could change, though, creating great difficulties world wide. Sound U.S. economic policies are a must. Let’s not forget the words of President Calvin Coolidge when speaking to a news trade group in 1925 about the role of the press in a modern, free-market, democratic America and shared warnings about the evils of propaganda: “After all, the chief business of the American people is business. They are profoundly concerned with producing, buying, selling, investing and prospering in the world.” The gravity of this statement has not changed in 100 years.

The Railway Track and Structures State of the Industry Survey

While we’ve covered a wide range of issues in this review, which the editors believe are important to anyone who is employed by either the railroad industry or one of the companies supporting it, we now focus on the results of the RT&S State of the Industry Survey conducted during the past several weeks. First, thank you to those who participated! For those who have never seen one or did not participate in the 2025 survey, we asked a series of questions that apply to a cross-section of the industry about its economic performance in 2025, with comparisons to 2024 and looking ahead to 2026. We will include detailed graphs in a special news story on our website, which will be live around the time you read this.

Overall, reports from our survey on business and planned spending for 2026 seem pretty good. For example, regarding the overall health of businesses, 55% of respondents said it is good, and 25% said it was excellent. As far as business activity in 2025 went, 30% said excellent and 40% said good.

Interestingly, with all the headwinds around U.S. trade policy, specifically tariffs, 40% of respondents said they had been impacted somewhat, and 35% said not really. The responses around the impact of interest rates and inflation were similar, with over 50% reporting that they had been impacted somewhat and about 25% reporting not really.

Respondents reported on the business outlook for 2026, with nearly 50% indicating the outlook is good and over 30% reporting the outlook is excellent. Regarding overall business activity, nearly 50% said business was better in 2025 than in 2024. Regarding business expectations in 2026, about 42% said 2026 would be better than 2025, while 50% said 2026 vs. 2025 would be flat.

The total spend on maintenance of way for 2025 was more than that spent in 2024 according to 45% of respondents, and about 42% said it was flat. Looking at MOW spending in 2026 vs. 2025, nearly 50% said there would be more spending and about 44% said spending would be flat in 2026. Our survey reported more specific data around the categories of planned maintenance spending, and that data will be presented in the charts accompanying our web story.

As is usually the case, business conditions, results, and forecasts are a mixed bag. Merger proceedings could mix it up even more. As long as consumer spending continues to improve, despite the drop in consumer confidence, this should bode well for the rail industry. However, the relatively high level of uncertainty around domestic and foreign economic and political policies, including trade policies, leaves us with a feeling of very cautious optimism (as opposed to cautious optimism) about economic and industry fortunes in 2026. To say the least, next year will be interesting!

Media

RELATED ARTICLES